Posts

- Generative AI for automating appeals

- A non-linear, inefficient example of an 'academia-to-industry' career path

- Double/debiased machine learning II: application

- Federated learning for clinical applications

- Coastal differences in artists' Instgram captions

- How many roads must a random walker walk down before it gets out of Reykjavik?

- Double/debiased machine learning I: theory

Generative AI for automating appeals

Focusing on architecture, May 2024

Motivation, via a comparison to the show 'Grand Designs'

One of my favorite light-hearted TV shows of late is the British home design marvel 'Grand Designs' (as I am writing this, it is free to stream on YouTube). The show - hosted by British designed Kevin McCloud - follows amateur, first-time builders as they set out to construct their own home. Almost without fail, the new builders go from being very excited about everything the new home will bring them, to miserable and downtrodden as delays and surprise costs push them to a breaking point. However, the episode (almost) always ends with a beautiful building, a beaming builder, and an uplifting narrative from the host about how this particular modern glass box represents a great triumph of the human spirit. And I tend to agree with him. Building your first home takes an admirable amount of bravery and perseverance. Additionally, the disparate backgrounds of the people on show sometimes result in truly unique and beautiful buildings.When watching the show, I often see parallels between the trials and tribulations faced by the home-owner-turned-project-managers and those faced when managing tech projects. I am not the first to draw such parallels - several participants on the show, as well as the authors of the project management book 'How Big Things Get Done' Bent Flyvbjerg and Dan Gardener, have noted the similarities between large projects in different mediums.

Flyvbjerg and Gardener takes this observation further by collecting and collating data from thousands of big projects across different sectors. Like the participants in 'Grand Designs', these projects also usually go over budget and over time despite being run by professionals. However, there a few common features of successful projects that the authors discuss. The feature most relevant to this post, is that successful (here, meaning on-time and on-budget) big projects are often made up of smaller repeated modules. One of the most memorable examples of the project management principle is the Empire State Building - an architectural marvel that was also a project management success. Each floor of the building is very similar. This similarity allowed worker to rapidly increase their speed at they built more floors, because they could learn from the mistakes they made on lower floors. As an individual contributor trying to build a new data science team in an established company, I am often thinking about how single projects can be used as smaller, repeatable building blocks to bring the team towards a grander vision.

One of these instances occurred while participating in meetings regarding how to best incorporate new generative AI technologies into our business practices. Here, it was important to balance good project management with minimizing risk to patients and maximizing benefit to the company when considering use cases. And there are no shortages of resources listing all the possible use cases of generative AI in healthcare. The problem is picking the best one to start with. If I were considering only project management, I would pick a simple app that used one foundation model, and one method for reducing hallucinations. This set up is common to many generative AI apps, and lessons learned in the simple case could be brought to other use cases. If I were only considering the minimal cost patients, I would probably start with some system that would be used only internally. Bain did the hard work of considering the maximizing business value part of the cost function and identified a few cases that stood out above the rest.

One of these use cases includes automating appeals. Part of their reasoning

comes from knowledge that payors automate denials with

the assumption that appeals are exceedingly rare. This means that denial are issued

liberally and many appeals are likely to provide adjustments. Additionally, automatic letter writing is not something that can easily be

achieved with simpler methodologies. The appeals use case does pretty well with other parts of the cost function too. Automating

appeals can have big impacts on revenue, but zero to low impact on patient care if something goes wrong. Lastly, the

architecture for an automated letter drafting system is like many other kinds of generative AI use cases. Therefore, choosing this as one of the first use cases can set

you up well to scale in the future.

One of these use cases includes automating appeals. Part of their reasoning

comes from knowledge that payors automate denials with

the assumption that appeals are exceedingly rare. This means that denial are issued

liberally and many appeals are likely to provide adjustments. Additionally, automatic letter writing is not something that can easily be

achieved with simpler methodologies. The appeals use case does pretty well with other parts of the cost function too. Automating

appeals can have big impacts on revenue, but zero to low impact on patient care if something goes wrong. Lastly, the

architecture for an automated letter drafting system is like many other kinds of generative AI use cases. Therefore, choosing this as one of the first use cases can set

you up well to scale in the future.

Generative AI Background

While an out-of-the-box LLM could probably generate a readable letter, it would likely hallucinate details about the patient or produce an overly generic letter if no modifications were made. We need to find a way to reduce these hallucinations and give the LLM access to specific information. This is why, at a high level, a generative AI system for automating appeals would have two main components: (1) a large language model (LLM) and (2) a method for retrieving documents relevant to the denial. Step 2 - the retrieval system - helps to address both the hallucinations and the lack of specific information. More specifically, step 2 refers to retrieval augmented generation (RAG). A process by which extra context is added to the prompt given to LLM to help it perform on specific tasks. From a data science perspective, setting up the retrieval system is a primary source of complexity in these apps.Another way to reduce hallucinations is to fine tune the foundation LLM model on data relevant to denial letters. Since both the RAG system and fine-tuning can help reduce hallucinations, we'll go more in depth into the differences between the two next.

RAG vs Fine-tuning

RAG: RAG (or retrieval augmented generation) is a process by which relevant context is added to the query to an LLM in hopes of getting more accurate and traceable answers. Retrieving context often relies on converting both the original query and the bank of contexts to vectors, matching the query-vector to the various context-vectors, and appending the contexts that are the most like the query. Performance of this retriever should generally be evaluated and periodically monitored. The documents available, the retrieval algorithm, and the vector embedding model are common thing to tweak during the process of building a RAG app.One of the benefits of RAG is that it is computationally fairly cheap and easy to update compared to fine-tuning. Additionally, if the relevant contexts change, all you have to do update your system is replace the documents, rather than retune the whole model. This is especially important in healthcare contexts where medical policies and contracts are changing on a yearly basis.

Fine-tuning: In general, fine-tuning refers to the process of taking a pretrained model and retraining it on a task different from its original purpose. When people talk about fine-tuning in generative AI applications, they are usually talking about taking an existing foundation model and training it to perform well in more specialized setting while retaining its general language capabilities, but you could also fine-tune the embedding models used in the RAG system (more on this later).

Fine-tuning has many of the same problems training other deep neural network models has. It can be computational very expensive to fine tune a model for a production application (even small LLMs have 10s of billions of parameters). While there are methods to minimize these costs (like parameter efficient fine-tuning, PEFT), they can still be prohibitive in some cases. Additionally, since fine-tuning will change the weights of the foundation model, it is wise to evaluate your final model both on its performance on the new task you are fine-tuning it on, and its general language accuracy too.

To summarize:

- Both RAG systems and fine-tuning can reduce hallucinations, but only RAG systems can provide the LLM with case specific documents.

- Both RAG systems and fine-tuning require high quality, context specific data.

- Fine-tuning requires more compute resources. These resources are spent on the tuning itself, and in the time it takes to re-evaluate the model after tuning.

- It is easier to update the corpus of documents for the RAG system when policies change than to retune an LLM.

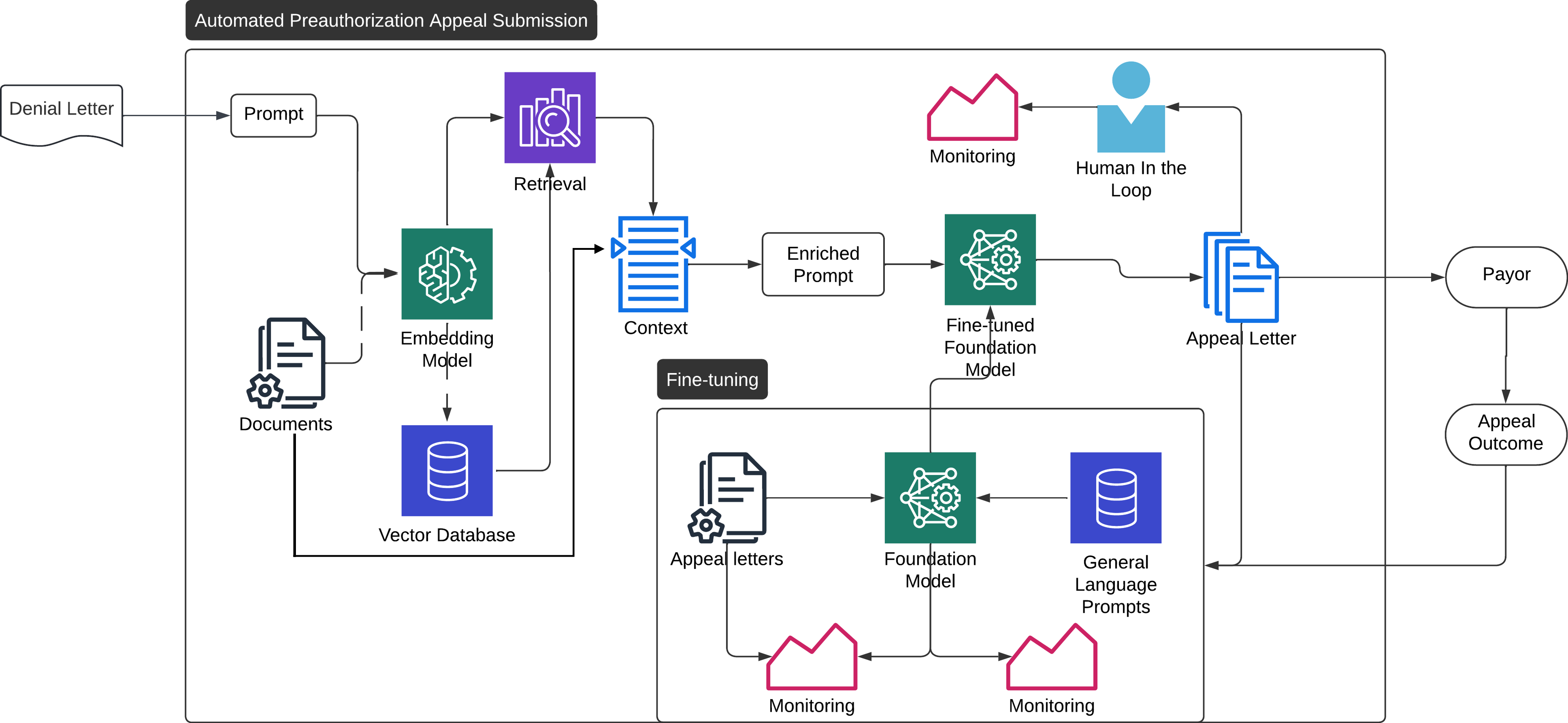

Example Architecture

Here, we show an example architecture for implementing a generative AI system for automating appeals.

- Denial letter comes in, is parsed to text, and embedded as a vector.

- Relevant information that can pulled directly from metadata are pulled.

- The denial letter embedding is compared to the information in the vector database. The best matches are pulled.

- The three pieces of information from the previous steps are combined into a query for the LLM

- The new query + context is sent to the LLM (fine-tuned or otherwise), which generates an appeal letter.

- The letter is stored for later evaluation.

- The letter is either reviewed by a specialist or sent directly to the payor.

- The payors response is recorded and monitored to assure the consistent performance of the system.

Vector database

The RAG system will need access to all the relevant information it would need to write the appeal letter. Some of this information can likely be passed directly to the app based on metadata about the denial, and some of it will need to be searched for. For example, medical notes unique to a specific patient could be pulled based on patient identifiers, while grabbing the specific part of the medical policy relevant to the procedure might require a search. The exact division will likely depend on the data ecosystem at a given institution. Any information that needs to be searched for will need to be parsed into chunks of text, encoded as a vector, and stored in a vector database. Most databases will be structured as some kind of hierarchical small world network, but sometimes more specialized topologies can be appropriate for some types of data. For example, this paper explored using a tree structure for internal company data, which is hierarchical.Embedding model

The embedding model is responsible for transforming the documents and queries to vector representations. Depending on the data the model is trained on, the model will likely have slightly different distances between similar words. Since healthcare is a pretty niche topic, I’d recommend starting with some kind of clinical embedding mode such as ClinBERT. This model is trained on clinical notes, if you are working with a vendor who provides embedding models specific to medical claims that would likely provide even better performance. You can also fine-tune embedding models on in house data to create more useful embeddings.Retrieval

How to quickly retrieve the ‘best’ context is remains an area of active research. The simplest and most common method uses a KNN or a similar algorithm to pull the ‘top-k’ nearest neighbors. FAISS or ANNOY are common tools for generating and searching embedding spaces. Using ElasticSearch together with FAISS or ANNOY can combine these vector searches with standard text or metadata-based searches. Ideally, you would also set up some kind of evaluation of the quality of the retrieved documents. A common way to evaluate these systems is to have raters look through results and mark the success of the retrieval based on a defined rubric.Foundation model and fine-tuning

Some consideration must be given to the foundation LLM at the start. In healthcare use cases, it is especially important to use foundation models that are HIPPA compliant and will not reuse queries in training sets, even if the data have already been deidentified. Additionally, fine-tuning requires setting up some kind of new task to train the model on more specific contexts. For this application, predicting the success of appeals from letters would be a good task, though it requires a large volume of appeal letters. In addition to the standard monitoring and evaluation required to fine-tune the foundation model, you will also want to set up some method of evaluating the general language capabilities of the fin- tuned model. There are several databases and packages of question-answer style prompts available for these purposes. While you're at it, you might as well throw in some extra monitoring for bias as well.Other parameters: In addition to privacy, there are other features of the foundation model to consider when selecting which one to start with:

- Number of parameters: This parameter is especially important if fine-tuning is going to be an integral part of your strategy. More parameters generally mean higher costs to tuning, though larger models might also often afford better performance.

- Maximum context size: Different foundation models have different limits for the largest prompt they will accept. Lower limits mean that you cannot include as much context in your query. While it might seem intuitive that more context would lead to better performance, that is not always the case. Regardless of your foundation model choice the amount of context to include is a parameter you can have to tune to improve performance.

- Transparency: Different foundation models adhere to different levels of transparency. More transparent models allow you to have more confidence in the model’s performance and blind spots. Additionally, if the model demonstrates bias in specific situations more information about the model can often lead to faster fixes. In healthcare, minimizing bias in anything impacting patient care (or payments, in this case) should be considered.

Conclusion

I've tried to provide the motivation, and the roadmap for an automated appeals system as a first step towards building robust generative AI for healthcare. This use case could bring in lots of uncaptured revenue for a company without risking patient care. Automating appeals can also help healthcare companies keep pace with payors. All while creating a nice template for future RAG applications. Now that we have laid out the vision and the plan, this would be the part of the 'Grand Designs' episode where the host foreshadows the setbacks to come and gives a knowing smile to the audience. While I do not currently have the benefit of hindsight, it is worth pointing out any generative AI app in healthcare with be difficult. The US healthcare system is extremely complicated, and any RAG system faces an uphill battle trying to parse between the subtle differences in contract language for the multitude of different payors, contracts, medical policies, etc. But I think it's worth the struggle. With an eye towards simplicity, modularity, and good project management, these apps can be technical and management successes.Other Resources

A non-linear, inefficient example of an 'academia-to-industry' career path

More specifically, a computational neuroscience to enterprise data science path, Feb 2023

When I started my PhD, I already suspected that I did not want to become a professor. However, I was very anxious about the limited knowledge

I had regarding non-academic career opportunities in my field. Due to this anxiety, I attended every career panel, read every Twitter thread, and consumed every

unsolicited piece of advice about post-PhD non-academic jobs as if they were gospel. These resources were useful, especially early in the process,

and I am grateful to everyone who offered their advice. However,

my job search still felt consistently surprising and out of my control.

When I started my PhD, I already suspected that I did not want to become a professor. However, I was very anxious about the limited knowledge

I had regarding non-academic career opportunities in my field. Due to this anxiety, I attended every career panel, read every Twitter thread, and consumed every

unsolicited piece of advice about post-PhD non-academic jobs as if they were gospel. These resources were useful, especially early in the process,

and I am grateful to everyone who offered their advice. However,

my job search still felt consistently surprising and out of my control.

My intention here is not to present a prescriptive approach to job searches but to add one example of the diverse range of non-linear paths that exist. My hope is that this account will offer some helpful tips for those looking for guidance or solidarity for those who feel confused about the process.

In this account, I will try to walk through the steps I took during the job search and share my observations and surprises along the way. As I am not an experienced writer, I will also include photographs of my cat Noodles to better convey my emotions during the process.

My background

It's important to acknowledge that I had a lot working in my favor to bring me to the PhD and industry science. For one, my dad worked in BioTech with a PhD, which made higher education and related fields an easy choice for me. Moreover, throughout the process I did not have to factor in any extra financial or caretaking responsibilities when making decisions.What I sought from a career path was job security, the ability to work in different locations, an environment that wasn't cutthroat, external validation of my work, good pay, fast-paced projects with clear endpoints (that were not papers), opportunities for creative problem-solving, the utilization of my existing skills, and a sense that my work was not inherently detrimental to the world. After considering my priorities, I concluded that a job in some kind of scienc-y industry (probably data science), outside of academia, could meet most of my criteria.

My timeline

I began my job search in earnest by interning at a university-affiliated research center (UARC) in June 2020. While I learned valuable skills during this internship, I ultimately decided to pursue a job that aligned better with my priorities. That being said, I believe UARCs are an excellent option for academics who enjoy their work but desire a more stable, higher-paying environment.In January 2021, after defending my PhD I chose to put off applying for jobs during the pandemic's peak by creating a more senior position in my current PhD lab. I also believed that I still had skills to develop before becoming a competitive candidate on the market, although this wasn't really true. I designed a data scientist position for my PhD lab that would let me do work as close as possible to the job I wanted, while still being part of academia.

I stayed in this academic data scientist position for 6 months, and then did my first non-academic job search in the summer of 2021 (upon reflection, this was also a very tumultuous time to be looking for tech jobs). I sent about 40 applications, got 5 interviews, and 1 offer at a Children's Hospital. This position was another academic data scientist position - not really the end point I had envisioned. I accepted the position, partially because I was feeling exhausted by the search process, but mostly because I anticipated that a new environment would provide additional learning opportunities.

After working at the Children's Hospital for about 6 months (now summer of 2022), I decided to start applying for jobs again. I applied to 10 positions, got called in for 1 interview, and received 1 offer. This time, the position was decidedly outside of academia, and seemed to meet most of the criteria I had. All in all, it took me 2 years, 50 applications, 6 interviews, and 2 offers to get my first non-academic job. Based on my conversations with other individuals who have transitioned from academia to industry, these numbers seem to be typical. The rest of the post is dedicated to giving more context to each of the steps I took to get there.

Understanding what you want

Even if you know that you don't want to stay in academia, understanding what you do want is a crucial first step. It may seem obvious, but deeply examining what you value in life, why you value it, and how your career fits into those values can be challenging. It may even force you to confront uncomfortable truths about yourself and reconcile conflicting desires. Online question prompts can help you get started, but most of my process involved conversations with friends and my partner.After I spent a lot of time confronting my own demons, the task of wading through a quagmire of job ads and career paths without an experienced mentor to guide me felt daunting. Part of me hoped that once I committed to a career path and made myself vulnerable enough to tell people my decision, a job would just materialize as an email in my inbox one day. But - unsurprisingly - that didn't happen, and the job search process continued to be challenging. However, the clarity I had about my values, paired with acceptance that they might change really helped me streamline my search and weather the process.

Understanding what's out there

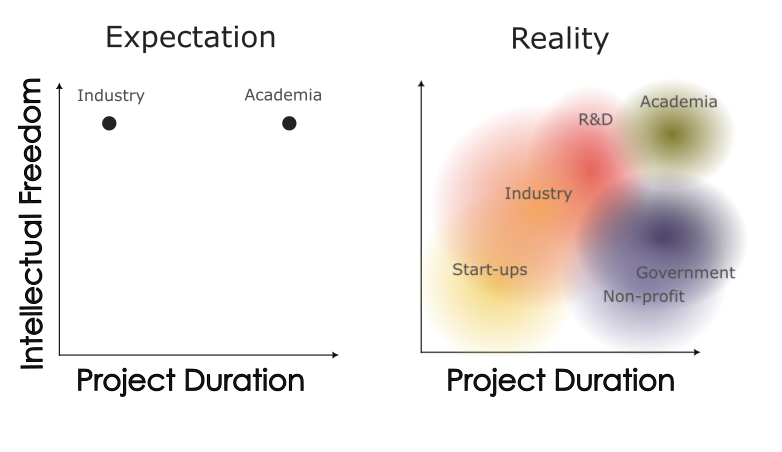

After getting some sense of what I wanted, it was time to see how different job titles and work sectors mapped onto those criteria. During the early stages of my PhD, I used to believe that the term 'industry' meant 'anything not academic'. I also held the misconception that the only distinguishing factor between the two sectors was that industry jobs were faster-paced and paid better. However, I have come to realize that this is not the case, and individuals outside of academia may find it perplexing if you describe their work as 'industry' when they actually work for a non-profit organization. Through the resources I have gathered since, I have created a more precise graphical representation of the job sectors. Characteristic of a data science, it is designed to resemble some kind of dimensionality reduction output. Here, the two most important dimensions are intellectual freedom, and project duration. Uncharacteristic of a data science, the plot involves no data, only vibes and assorted perspectives I've collected over time. The first graphic describes my early impressions of industry early in my PhD. I formed my ideas based on interactions with industry scientists who focused on a narrow type of R&D

research. These scientists typically worked for well-funded R&D divisions and believed they had as much intellectual freedom as they would have had in academia. The second graphic

reflects my current understanding, which has evolved. Notably, each sector is represented by a density rather than a point estimate (the text placement was chosen for visualization

purposes and does not reflect the density centroid). As a result, there is considerable overlap between categories. While some industry, government, or non-profit positions offer as

much intellectual freedom as academia, many do not. The same is true for pace.

The first graphic describes my early impressions of industry early in my PhD. I formed my ideas based on interactions with industry scientists who focused on a narrow type of R&D

research. These scientists typically worked for well-funded R&D divisions and believed they had as much intellectual freedom as they would have had in academia. The second graphic

reflects my current understanding, which has evolved. Notably, each sector is represented by a density rather than a point estimate (the text placement was chosen for visualization

purposes and does not reflect the density centroid). As a result, there is considerable overlap between categories. While some industry, government, or non-profit positions offer as

much intellectual freedom as academia, many do not. The same is true for pace.

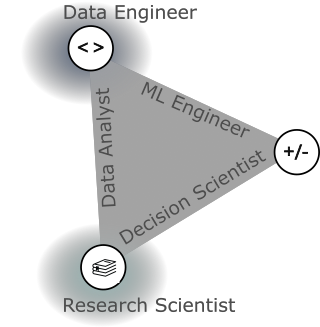

In each of these sectors, there are various job titles related to 'data science'. While the majority of postings will list 'data scientist' as the job title, most could be described as a more granular level by one of several categories. The book 'Build a Career in Data Science' uses a graphical representation to illustrate these different jobs based on their skillsets. I have recreated this graphic below. The three corners represent three common types of skills valued in data science: math/stats (+/-), coding/databases (<>), and domain knowledge/communication (the stack of books). Different jobs emphasize different combinations of these skills. For instance, the 'decision scientist' data scientist depends mostly on communication or domain expertise and math/stats skills, while the 'data analyst' data scientist relies more on databases and domain expertise, and the 'MLOps' data scientist relies heavily on coding/databases and math/stats. Additionally, there are some data science-adjacent positions that heavily rely on one of these types of skills (i.e., research scientist or data engineer). The purpose of this post is not to provide a detailed description of each of these jobs, but to give a starting point to dive in further. The book from which this graphic was taken is an excellent resource to learn more.

When I began my search for data science jobs, I was overwhelmed by the variety of skill sets listed in different job ads. This led me to the false assumption that I needed to be an

expert in all these skills to be a competitive candidate for any data science job. However, the key takeaway from the graphic is that you do not need to excel in all the skills

to get a job in data science. Instead, you can leverage your existing strengths to find a data scientist role that is a good match for you.

When I began my search for data science jobs, I was overwhelmed by the variety of skill sets listed in different job ads. This led me to the false assumption that I needed to be an

expert in all these skills to be a competitive candidate for any data science job. However, the key takeaway from the graphic is that you do not need to excel in all the skills

to get a job in data science. Instead, you can leverage your existing strengths to find a data scientist role that is a good match for you.

It's worth noting that data science is a popular title right now, and some companies may use it to refer to a wide range of positions to attract top talent. Being selective with the job ads you apply to based on the listed skills can help cut through some of this noise. Furthermore, if a job ad requires expertise in all aspects of data work, it could be a red flag indicating that the company does not fully understand the diverse range of roles required to effectively use data.

Understanding skillsets for data science

I eventually decided to pursue a career as a decision scientist/data scientist. As shown in the previous graphic, this role places more emphasis on math and domain knowledge rather than coding/database skills, but companies often have specific skill requirements for these positions.To better understand the necessary skills for this role, I have compiled a list of skills that I believe are common across different data science job postings. I categorized them into three groups: skills that I acquired during my PhD without consciously trying to develop them, skills that I intentionally worked on during my PhD, and skills that I think would be difficult or impossible to gain solely through a PhD program.

Things I had gained by getting my PhD without really trying

- project management

- breaking down complex problems into actionable steps

- statistics

- experimentation and hypothesis testing

- biomedical domain expertise

- coding in Python or R (I realize that this is not a given for everyone)

- the ability to learn new technical skills and methods

- the ability to select between different methods

- coming up with new projects and next steps

- coding in SQL

- some advanced machine learning and statistics (note that this says some, not all)

- exposure to JavaScript and web apps (most jobs don't expect you to know JavaScript, but it was useful to understand how a web app worked)

- some best practices in coding: github, packaging python code, unittesting and reproducible machine learning pipelines (like MLFlow)

- Specific database management tools that cost money Universities aren't willing to pay for (Snowflake, AWS, etc.)

- How to prioritize projects based on business value*

- Knowledge of different business models (healthcare is wild)*

- Knowledge of how to design projects that provide value to someone outside of a University (i.e. marketing, accounting, etc.)*

Understanding industry's perception of academics

At this point, I knew both what jobs I was interested in and roughly which ones I had the skills to do. However, me deciding I had those skills and me convincing other people I had them were two different things. I had to learn a lot about how people in other sectors perceived academics to be successful on the market.During my PhD program, most of the information I received about industry jobs was presented at events sponsored by the program. These events had a generally positive outlook on job prospects after graduation and emphasized that PhD candidates had many desirable skills, and would have many options after graduating. While this was not inaccurate, it gave me the impression that most companies explicitly sought out PhD graduates and understood what a PhD entailed. This impression was not entirely true in practice. While some companies, particularly R&D departments, have a history of hiring academics and are more familiar with interpreting academic accomplishments, this is less common in the business/enterprise data science field.

While most people in industry recognized that PhDs foster independent work and decision-making. I found that I had to work harder to convince companies of my technical skills, project management abilities, and communication skills. Additionally, industry employers expected PhD graduates to have no business knowledge, to have trouble prioritizing the interests of the company over their own professional development, and to have trouble working with teams at a fast pace. These were significant challenges I had to overcome during the application process. In one informational interview, I had to make 3 attempts to convince the person I was talking to that despite my degree being in neuroscience, I had no experience or interest in doing bench science at the company. I tried to address these issues by learning the appropriate language to use in resumes and interviews (which I will discuss in more detail later), but I am still working on the best way to position my PhD as relevant experience.

I also held misconceptions about the appropriate level at which to apply. A professional mentor had informed me that companies would consider my PhD as work experience and that I could apply to more senior positions. However, I discovered that this was only partially true. While some positions considered my PhD work as technical experience (i.e., X years of experience with machine learning models), it was not viewed as actual work experience (i.e. X years of experience as a data scientist). "Senior data scientist" positions typically require experience in a for-profit company, preferably one with a similar business model as the hiring company. The more realistic expectation is to begin with an entry-level data scientist position and advance to a senior level after demonstrating an ability to prioritize the company's interests. For some people this can happen quickly (in about a year).

Finally, I had a significant misunderstanding about what was expected from job application materials. My past experience with marketing myself was mostly through personal statements for school, which focused heavily on why I was interested in pursuing further education and why I was passionate about a particular program. However, I quickly learned that this approach did not work for job and internship applications. Instead of trying to convince employers of my commitment to a particular field, I needed to focus on showcasing what I could offer to their company. It became apparent that employers are primarily interested in how an applicant can be valuable to their organization, rather than why the applicant wants to work for them.

Informational interviews and networking

Almost every resource I found emphasized that informational interviews and networking was very important for landing the first job in a field. Unfortunately, I found this to be true. I had over 20 informational interviews during my PhD and job search. Some were at early stages when I was still figuring out what to do, and others were directly tied to specific job ads. While I love hearing about people's experiences, I am generally nervous to talk to them about it directly and prefer to gather perspectives from books and blogs. Overall, I found the process of informational interviewing quite taxing - however many of them gave me useful information or, in a minority of cases, a referral for a job.There are a lot of resources available online for informational interviews. I also used my school's career center as a resource on this topic. Much of the advice on networking is tailored to different levels of familiarity, such as reaching out to a friend, an acquaintance, or a stranger.

An important note on LinkedIn: while academics do not rely on it, industry 100% does. I learned that to show up on recruiters' feed, you need to have some basic engagement with the app. I followed some popular pages like sklearn, pytorch, etc., and liked their posts to boost my visibility. I have no way of knowing if this was helpful.

In my search, I reached out to strangers very infrequently and instead relied on people I knew from school in one way or another. This approach was not recommended to me, but it is what I was most comfortable with. I was pleasantly surprised to learn that I passively benefited a lot from my undergrad and grad school's network. I had one interview that resulted from a referral from a friend, but all five others had team members that went to either my undergrad or graduate university. Even though I did not reach out to these people for informational interviews, I think I benefitted from baseline credibility that I gained from sharing an educational background. I think I was fortunate to have gone to schools with some name recognition that placed a lot of people in tech. This observation is what motivated me to so say that networking mattered for me. While most of my interviews weren't tied to me reaching out to someone at the company, all involved some kind of personal connection to my background.

At their best, informational interviews are great ways to get energized about a position and learn more about a job. They might even lead to referrals and eventually offers. I tried my best to embody this attitude as I reached out to people to network.

Internships

Of the individuals I know who moved straight from a neuroscience PhD to a data scientist role (n=3), all of them landed their first job by starting with an internship. There are similar paths through bootcamps and fellowships, but I do not have any experience with those. When I began exploring internship opportunities, I was not aware of how common it was for companies to hire interns from graduate school. I limited my search to 3 or 4 places where I had direct connections, but I later discovered that internship searches can be quite broad, with many opportunities available on platforms like LinkedIn.Another noteworthy aspect of internships is that the expectations for them are different from those for full-time positions. Internship programs typically seek interns who can make meaningful contributions in a short amount of time, which makes it crucial to present oneself from the perspective of what one can offer. Companies are less likely to select candidates who require significant training. In contrast, when filling full-time positions, companies may be willing to invest in training to help a candidate gain skills if they are otherwise a good fit for the company. Additionally, some companies may even have less competition for full-time positions than internships.

Resumes and Cover Letters

When I first started applying for jobs, I sought help from my University's career center for guidance on crafting my application materials. At first, I found their advice to be very beneficial, and my application materials significantly improved. They helped me make more specific resume items, and told me to always customize my resume and always submit a cover letter. However, I eventually encountered conflicting advice from different advisors, leaving me unsure about which changes to make. Eventually, I realized that there was no "perfect" resume, and there would always be some element of chance involved in trying to appeal to the hiring manager.When applying to large companies, it is common for your resume to be screened by a computer program that checks for your suitability for the job. These programs aim to match elements of your projects to the job description, although they can sometimes make egregious errors. To tailor my resumes to each position, I used a tool provided by my university called ResumeTargetted. This tool helped to identify key words and phrases to include in my resume to make it a better match for the job. If you don't have access to a similar tool, you can still try to use the language and terminology from the job ad in your application materials. I have no idea if this process of changing language was helpful or not, but I found it comforting to have some kind of formula to follow when making my resumes.

Interviews

By the numbers

Advancing through job interviews is a highly unpredictable process, and unfortunately, you have to go through many of them before knowing whether you're competitive. The rough rule of thumb I was given for full-time job applications was an application-to-interview ratio of 10 to 1. If you've applied to 20 jobs and haven't received any responses, it might be worth revisiting your application materials. However, if you've only applied to about 10 jobs, you might just have to keep at it for a bit longer.Similarly, I was told that it takes an average of about 5 interviews to receive a job offer. If you're consistently getting stuck at a specific point (e.g. technical, behavioral), it's worth revisiting your approach. However, if you're making it to the final stages of interviews and not receiving an offer, it's likely just a matter of bad luck. If you persist, you will likely find something eventually. I found this easier said than done - the amount of rejection I faced was often devastating. I was grateful to have a strong support system and non-work activities to help sustain me.

For technical interviews specifically, many companies use services like LeetCode to generate questions. Many applicants spend a lot of time studying these. I purposefully avoided companies that used these services, and therefore have no insights on how to prepare for them.

Preparing

Another thing I learned while interviewing is that many companies expect candidates to fully understand their business model at the oustset and not to learn it on the job. During an interview with a healthcare startup, I gave a presentation on some analyses I had done on a subset of their data. My conclusion was that the company was underrepresented in an area that needed their service. Someone asked me how I would measure if my plan was successful for the business if enacted - a question I found very confusing. To me it seemed obvious: more people needing the service == more more people using the service == good for company. It turned out that this company mostly sells to other companies rather than people so my original logic does not pan out. If I had known this beforehand, I would have structured my proposal differently.I'm still trying to figure out how to gain this knowledge reliably, but a few things have helped. For example, the website CrunchBase provides basic information on companies' finances and links to news and articles about them. You can also look for public earnings reports or quarterly updates that companies provide publicly. Additionally, exploring a company's website can sometimes provide clues about which customers are important to them and which new products they are focusing on.

Asking questions

Not all of this information needs to be figured out before the interview. Generally, asking questions about the financials of the company is encouraged, and not a taboo subject as I had thought. A friend who is a software engineer encouraged me to ask these types of questions to get a better understanding of the business. For start-ups, he suggested: (1) How much runway do you have? This basically translates to how long will you be able to pay me if the company doesn't get more funding? (2) When do you expect to be profitable? I asked this once and got an answer that started with 'Oof', but the question was still answered in good spirits. For public companies, he also encouraged me to ask any and all basic questions I had about the business model. Do you primarily sell to clinicians, hospital, or patients? What are your goals for this quarter? etc. Essentially, very few questions were actually off-limits, and I found that whenever I did ask questions about the business model or the company's future, my interviewers responded well. I never got the sense that interviewer thought I sounded unqualified based on the questions I asked.Conclusions

When I have conversations with people about making a career change, they often ask me, "If there was one thing you wish you had done in your PhD that would have better prepared you for getting a data science job, what would it be?" I believe the one thing that would have helped me with this process was letting go of the idea that my career path was entirely within my control and that a smooth and linear path meant I had done everything "right." My PhD experience unexpectedly helped me in many ways, and many things I thought would lead to an "easy" job did not work out. I also had to take short-term steps that seemed like a step "backward" or "sideways" and trust that they would ultimately lead me to a more fulfilling place. Currently, I have found a career path that meets many of my needs and supports the flexible lifestyle I want in other domains. I fully expect that this may change again in the future. What I wish I had done during my PhD is internalize that all of these experiences are normal.

Other resources

These were some other resources I used during the job search that helped me appreciate the diversity and non-linearity or career paths out there.- Build a Career in Data Science book and podcast

- Dr. Tanya Jonker's blog

- Dr. Lily Jampol put on the career event that I found most true to my experience

Double/debiased machine learning II: application

Application of the DML method to simulated data, with code, December, 2022

What is double/debiased machine learning?

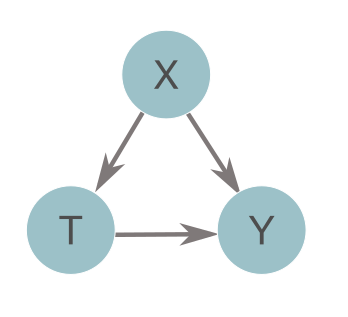

Double or debiased machine learning (DML) is a method for estimating causal treatment effects from complex data [1]. In biomedical settings, treatment effects can tell you how much the administration of a given medication (T) can decrease the risk of some adverse event (Y) while accounting for other confounding variables (X). Essentially, it isolates the arrow connecting T to Y in the diagram below. At a population level, this value is called the average treatment effect (ATE), or \(\theta\). At the individual level, this value is called a heterogeneous treatment effect, conditional average treatment effect (CATE), or \(\theta(X)\) (the rest of this post will discuss CATEs rather than ATEs). If causal assumptions are met [2], DML can provide us with accurate estimates of treatment effects, with confidence intervals, without making strict assumptions about the form of the data. The lack of strict assumptions is achieved by leveraging machine learning to estimate confounding effects (the X to Y and X to T arrows above).

In short, the method estimates treatment effects with a 3 step algorithm:

If causal assumptions are met [2], DML can provide us with accurate estimates of treatment effects, with confidence intervals, without making strict assumptions about the form of the data. The lack of strict assumptions is achieved by leveraging machine learning to estimate confounding effects (the X to Y and X to T arrows above).

In short, the method estimates treatment effects with a 3 step algorithm:

- Estimate the mapping from X to Y with ML

- Estimate the mapping from X to T with ML

- Regress the residuals from (1) onto the residuals from (2). The results of this is the treatment effect

Data generating process

We're now going to walk through an example application of DML to a simulated dataset. We will use the following equations to generate our dataset: $$ {Y=T\times \theta(X)+\langle X| \gamma \rangle + \epsilon,} $$ $$ {T \sim Bernoulli( f(X) ), f(X) = \sigma( \langle X| \beta \rangle) + \eta} $$ $$ {\theta(X) = e^{2 \times X_1}} $$ Essentially, these equations are saying the Y is a linear combination of variables from X plus \(\theta\) times the treatment, and T is a binarized, linear combination of other variables from X. Lastly, \(\theta\) is an exponential function based on the first column of X. More specifically,- Y the treatment effect times a binary indicator of treatment, plus a linear combination of variables from X, plus some noise. \(\gamma\) selects the and weights the columns of X included in the simulation.

- T is the binary treatment variable. It is calculated by passing a linear combination of variables from X, weighted and selected by \(\beta\), into a sigmoidal logit function \(\sigma\).

- \(\theta(X)\) is an exponential function of the first column of X times 2

- \(\gamma\), \(\beta\) have 50 nonzero elements, which are drawn from a uniform distribution between -1 and 1

- \(\epsilon\), \(\eta\) are noise terms uniformly distributed between -1 and 1

- X is a matrix with entries uniformly distributed between 0 and 1

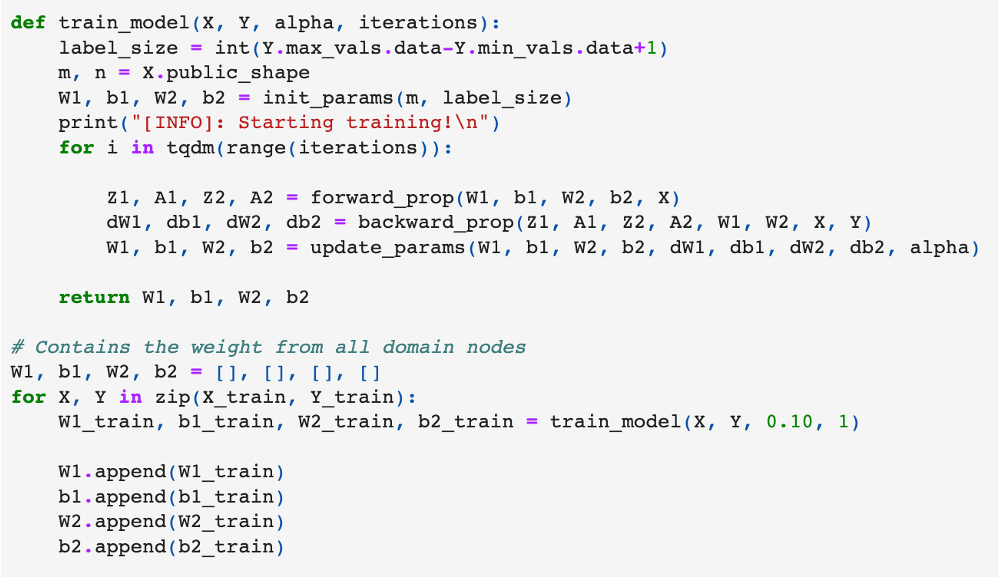

We can simulate our data in Python with the code below:

import numpy as np

def get_data(n, n_x, support_size, coef=2):

"""

heterogeneous CATE data generating process

params:

:param bin_treat: a boolean indicating whether the treatment is binary (true) or continuous (false)

:param n: the number of observations to simulate

:param n_x: the number of columns of X to simulate

:param support_size: the number of columns of X that influence T and Y. Must be smaller than n_x

:return: x, y, t, and cate, the features, risk, treatment, and treatment effect

"""

# patient features

x = np.random.uniform(0, 1, size=(n, n_x))

# conditional average treatment effect

cate = [theta(xi, coef=coef) for xi in x]

# noise

u = np.random.uniform(-1, 1, size=[n, ])

v = np.random.uniform(-1, 1, size=[n, ])

# coefficients

support_Y = np.random.choice(np.arange(n_x), size=support_size, replace=False)

coefs_Y = np.random.uniform(-1, 1, size=support_size)

support_T = support_Y

coefs_T = np.random.uniform(-1, 1, size=support_size)

# treatment

log_odds = np.dot(x[:, support_T], coefs_T) + u

t_sigmoid = 1 / (1 + np.exp(-log_odds))

t = np.array([np.random.binomial(1, p) for p in t_sigmoid])

# risk

y = cate * t + np.dot(x[:, support_Y], coefs_Y) + v

return x, y, t, cate

>

def theta(x, coef=2, ind=0):

"""

exponential treatment effect as a function of patient characteristics (x)

:param x: the feature data for a single observation (size 1 x n_x)

:param coef: the coefficient in the exponential function (default 2)

:param ind: an integer indicating which column of x to use in the exponential function (default 0)

:return: the treatment effect for a given observation

"""

return np.exp(coef * x[ind])

>

n = 5000

n_x= 100

support_size=50

x, y, t, cate = get_data(n, n_x, support_size, coef=2, bin_treat=True)

x_train, x_test, y_train, y_test, t_train, t_test, cate_train, cate_test = train_test_split(x,

y,

t,

cate,

test_size=0.8)

>Train T model

You can really train your model however you want, we're just going to define a simple random forest model here. econML has the benefit of working with GridSearchCV objects and taking care of Y and T hyperparameter tuning for us (if you aren't familiar with GridSearchCV, check out its docs).

from sklearn.ensemble import RandomForestClassifier

from sklearn.model_selection import GridSearchCV

# parameters for forest

params = {

'max_depth': [5, 10],

'min_samples_leaf': [2, 4, 10],

'min_samples_split': [2, 4],

'n_estimators':[400, 1000]

}

t_mdls = GridSearchCV(RandomForestClassifier(),

params,

cv=5)

t_mdl = t_mdls.fit(x_train, t_train).best_estimator_

>

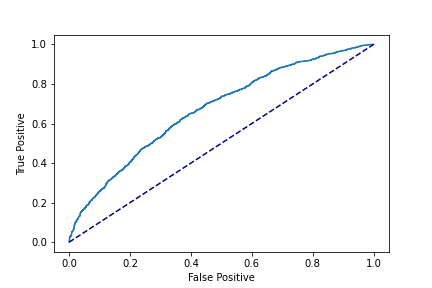

from sklearn.metrics import roc_auc_score, roc_curve

import matplotlib.pyplot as plt

# evaluate T

import matplotlib.pyplot as plt

pred = t_mdl.predict_proba(x_test)[:,1]

fpr, tpr, _ = roc_curve(t_test,pred,drop_intermediate=False)

roc_auc = roc_auc_score(t_test,pred)

plt.plot(fpr, tpr)

plt.plot([0, 1], [0, 1], color='navy',linestyle='--')

plt.xlabel('False Positive')

plt.ylabel('True Positive')

>

print(roc_auc)Output:

0.6471481

Our T model AUC is 0.65, which is far from impressive. But remember,

we can (theoretically) get good CATEs even if our T model performance isn't great, so let's keep going.

Train Y model

We can do the same thing for the Y model. Let's use a gradient boosted classifier to mix things up.

# fit y

from xgboost import XGBRegressor

# parameters for forest

params = {

'max_depth': [5, 10],

'learning_rate': [0.1, 0.01, 0.05],

'n_estimators':[50, 400, 1000]

}

y_mdls = GridSearchCV(XGBRegressor(),

params,cv=5,

n_jobs=-1)

y_mdl = y_mdls.fit(x_train, y_train).best_estimator_

>

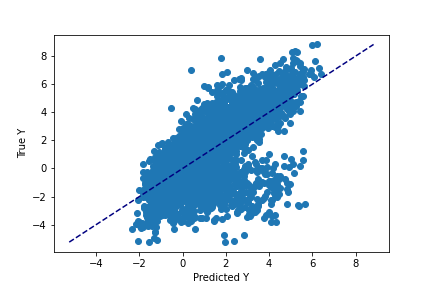

# evaluate Y

pred = y_mdl.predict(x_test)

plt.scatter(pred, y_test)

lims = [

np.min([pred, y_test]), # min of both axes

np.max([pred, y_test]), # max of both axes

]

plt.plot(lims, lims, color='navy',linestyle='--')

plt.xlabel('Predicted Y')

plt.ylabel('True Y')

>

np.mean(np.abs(pred - y_test) / y_test)Output:

0.4681890

Similarly, we get mediocer performance when estimating Y. Our values have a bias of about 47%, meaning that if our true Y value was 10, our model would be guessing 15.

Train the estimator

We can now pick an estimator. econML has 3 main estimators that provide confidence intervals. The 'SparseLinear' and 'Linear' estimator will only work if you have many more observations than variables (see this table for comparisons of different estimators). For a lot of real-world data, this is not the case, therefore we will use the last remaining option: CausalForest estimator [4]. Like random forest models, this estimator also has the benefit of being able to estimate non-linear treatment effects in a piece-wise fashion.

# dml

from econml.dml import CausalForestDML

est = CausalForestDML(model_y=y_mdl, model_t=t_mdl, cv=5)

>Also similar to 'RandomForestClassifiers' in scikit learn, the 'CausalForest' estimator has many other parameters. If you're familiar with random forests many of these parameters will be familiar: the number of trees to include, the maximum depth of those trees, etc. The big exception in parameters between causal forests in econML and sklearn is that econML forest has no class weighting option. This is because the causal forest method makes use of a specific weighting strategy already [4].

Additionally, the econML estimator can't be used as input into sklearn's 'GridSearchCV' or 'RandomSearchCV' functions. However, we can use econML's own hypterparameter tuning function 'tune'. Rather than evaluating parameter performance across cross-validated folds of data, this fucntion uses out-of-bag scores on a single, small forest.

# parameters for causal forest

est_params = {

'max_depth': [5, 10, None],

'min_samples_leaf': [5, 2],

'min_samples_split': [10, 4],

'n_estimators': [100, 500]

}

est = est.tune(Y=y_train, T=t_train, X=x_train, params=est_params)

est.fit(Y=y_train, T=t_train, X=x_train)

Evaluation

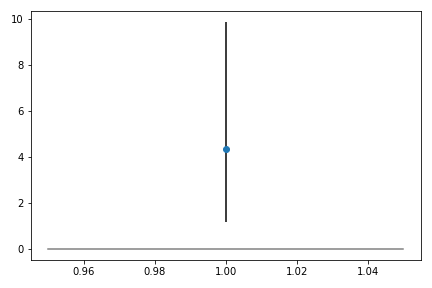

Before we evaluate the model performance, we're going to talk about viewing individual CATEs and their confidence intervals. In a clinical application, these values are what would be used in the decision-making process surrounding which interventions to use for a given patient.

# get individual CATES

patient_idx = np.random.randint(np.shape(X_test)[0])

# get cate

cate = mdl.effect(X_test[patient_idx:patient_idx+1,])[0]

# get cate CI

lb, ub = mdl_dict[name].effect_interval(X_test_clean[patient_idx:patient_idx+1,], alpha=0.05)

# plot CATEs with CI for individual patients

plt.figure(figsize=(8,6))

plt.errorbar(1, cate, yerr=ci,

fmt="o", ecolor='k', zorder=1)

plt.tight_layout()

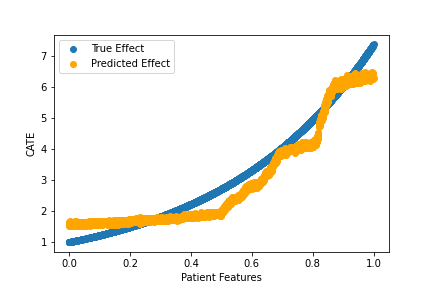

> This plot indicates that for this patient, the model estimates that adding the treatment will increase the outcome measure by 4, though it has a wide confidence interval, spanning about 1 to 10.

This plot indicates that for this patient, the model estimates that adding the treatment will increase the outcome measure by 4, though it has a wide confidence interval, spanning about 1 to 10.

Now we can move on to evaluation. How'd we do? Since this is simulated data, we can see how well our estimated treatment matches the true effect.

# plot

plt.figure()

plt.scatter(x_test[:,0], cate_test, label='True Effect')

plt.scatter(x_test[:,0], cate_pred, color='orange', label='Predicted Effect')

plt.xlabel('Patient Features')

plt.ylabel('CATE')

plt.legend()

>

np.mean(np.abs(cate_pred - cate_test) / cate_test)Output:

0.1577856

We did pretty well! Notably, we did pretty well even though our T and Y models had mediocre performance. Here our model bias is about 16%, substantially lower than the bias for Y.

What are the limits of this good performance though? What is the minimum number of samples? What happens when we add more variables, or more noise?

This paper [3] shows that DML (and all causal estimation methods) do better with more samples, fewer variables (though DML does better than other methods when the number of columns of X > 150),

fewer confounding variables, and weaker confounding.

Evaluations with empirical data

We can use simulations to demonstrate that DML can perform pretty well in some messy situations - like when we get mediocre predictions of T and Y. However, all these demonstrations rely on the fact that we know the true value of \(\theta(X)\). In real-world settings, this is not realistically possible, so how do we evaluate our models? I've been exploring a few options:- Consistency in CATE and ATE estimates: While this method is more of a validity check than an evaluation, it is considered best practice for any method estimating conditional average treatment effects (CATEs, which were the subject of this post). The idea is that you bin your heterogeneous treatment effects into a few bins and recalculate average treatment effects within each bin. While we didn't discuss them here, average treatment effects (ATE) are a sample level equivalent of the conditional averages. If your ATE and CATE distributions are similar, you can have more confidence that your CATE estimates are not spurious.

- Benchmarking and medical knowledge: To some extent, we can leverage medical knowledge to confirm that our CATEs are in the right neighborhood. For example, we have substantial scientific evidence that aspirin can lower people's risk for heart attack. Therefore, if our mean CATE is ~20%, indicating an increase in risk, we can be reasonably sure that the model isn't performing well.

- Improved prediction: we can also put the evaluation back into a prediction-based framework. Mathematically, a patient’s true risk Y(t) = Y(t-1) + CATE. If our predictions get better with the addition of the CATEs, we can at least conclude that our prediction is useful. It’s important to note that 'useful' is not the same as 'accurate’ and is not a validation of the causal assumptions of the model.

References

- Chernozhukov, V., Chetverikov, D., Demirer, M., Duflo, E., Hansen, C., Newey, W., & Robins, J. (2016). Double/Debiased Machine Learning for Treatment and Causal Parameters. http://arxiv.org/abs/1608.00060

- Rose, S., & Rizopoulos, D. (2020). Machine learning for causal inference in Biostatistics. In Biostatistics (Oxford, England) (Vol. 21, Issue 2, pp. 336–338). NLM (Medline). https://doi.org/10.1093/biostatistics/kxz045

- McConnell KJ, Lindner S. Estimating treatment effects with machine learning. Health Serv Res. 2019 Dec;54(6):1273-1282. doi: 10.1111/1475-6773.13212. Epub 2019 Oct 10. PMID: 31602641; PMCID: PMC6863230.

- Oprescu, M., Syrgkanis, V., & Wu, Z. S. (2018). Orthogonal Random Forest for Causal Inference. http://arxiv.org/abs/1806.03467

Federated learning for clinical applications

A primer for the data-governance/privacy curious, October, 2022

Data Privacy and Governance in Clinical Machine Learning

Clinical machine learning seeks to ethically improve patients’ outcomes in healthcare settings using complex data and statistical methods. Generally, many of these statistical methods involve learning associations between various real-world measures – like the risk of disease X and the amount of protein Y. The accuracy of these learned associations tends to increase as you get more data. Additionally, newly developed methods with the potential to solve unique problems, also tend to require more data to get accurate results. Likewise, models targeting rare conditions require, unsurprisingly, even more data. This is not to say that data is the only issue facing clinical machine learning, but it certainly an important factor in the field's progress. However, the process of collecting storing, and distributing data, especially medical data, is extremely difficult and often not incentivized. We’re going to briefly discuss two important aspects of the data ecosystem -- data privacy, and data governance. We’ll then describe a technical advancement in model training – federated learning – that allows for model development in an ecosystem focused on maintaining decentralized data governance [1].Data Privacy: Medical data are often highly sensitive in nature and breaches in privacy could cause significant harm to patients. Additionally, it is becoming clear that simply anonymizing data – i.e. removing patient names and unique identifiers – might not be enough to ensure privacy. We now know that patient faces can be reconstructed from medical scans, making the patient's identifying features and the features used in modeling inseparable in these applications[2]. These issues make hospitals hesitant to share data, even with other hospitals, and put high security requirements on any server seeking to host shared data from multiple sources.

Data Governance: Collecting, storing and maintaining large datasets takes massive amounts of work. In academic settings, providing these datasets as a resource to the public is not incentivized; time spent writing original research papers is considered more useful. Similarly in industry or non-profit settings, institutions often want to retain control of their data efforts because of the resources invested into them. While it would also benefit progress to incentivize sharing, finding ways to work within current incentive structures for data governance can help build larger multisite datasets quickly.

Both data privacy and data governance are necessary parts of the data ecosystem that unfortunately disincentivize institutions to share their data or contribute them to larger data lakes. Making them both an important safeguard and a barrier to progress. If there were a way to decentralize model training such that institutions could retain control of their data, and modelers could incorporate that data into their work, clinical applications could advance without sacrificing privacy or drastically changing incentives. This decentralization is the promise of federated learning.

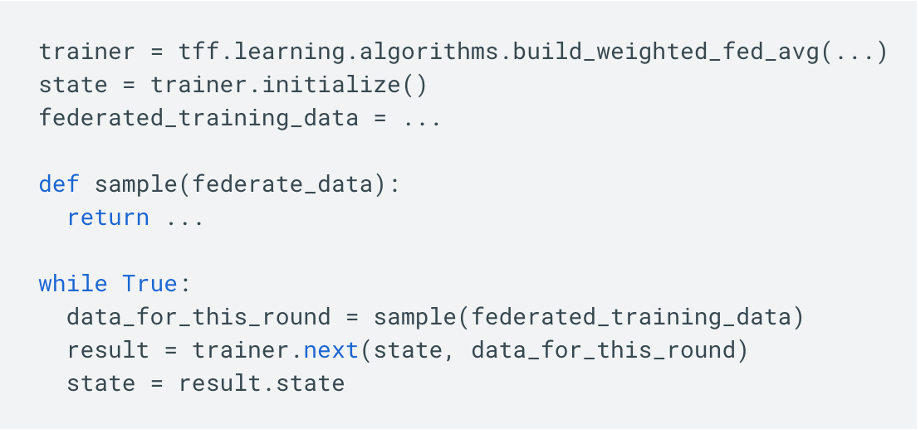

Federated Learning Definition

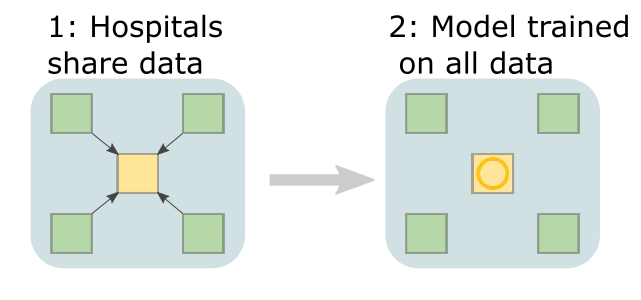

Federated learning achieves decentralization by training individual models at each participating institution and then aggregating the parameters from each local model to create one global model. This way, data are never passed between sites, only parameters are. Before going into a bit more depth on the definition, lets visualize a typical centralized learning pipeline (visualization adapted from [1]). Data from multiple hospitals (green squares, called 'nodes') would need to be shared with some central server (yellow square, called 'aggregate node' or 'central node'). Assuming that was successful, you could then train a model on data from every site at that centralized server. Seems simple, but we’ve already discussed why data sharing might not be a sustainable solution.

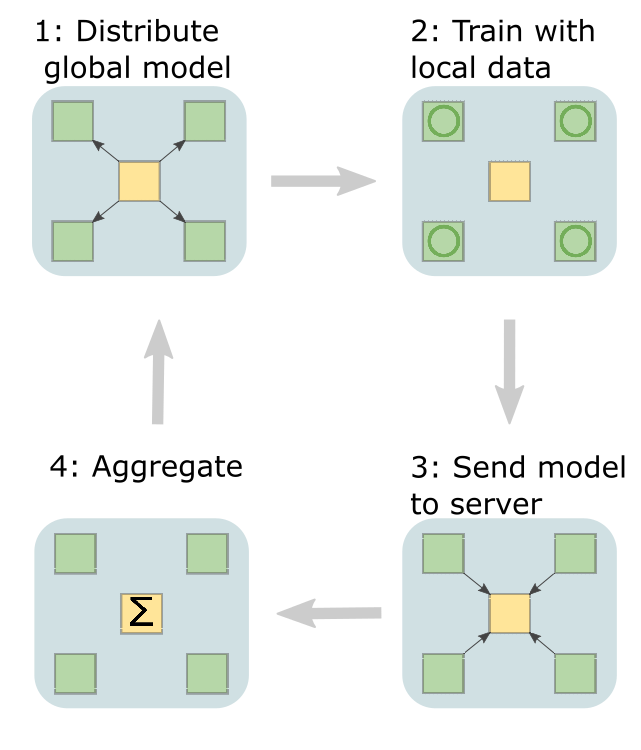

Let instead look at the schematic for federated learning (visualization adapted from [1]).

Data from multiple hospitals (green squares, called 'nodes') would need to be shared with some central server (yellow square, called 'aggregate node' or 'central node'). Assuming that was successful, you could then train a model on data from every site at that centralized server. Seems simple, but we’ve already discussed why data sharing might not be a sustainable solution.

Let instead look at the schematic for federated learning (visualization adapted from [1]).

The first step is for the central server to share a model with each node. Then, models are trained locally before sending their parameters back to the central server.

The central server will then aggregate all the parameters, before sending the updated model back out to each hospital. This repeats until the model is trained.

To formalize this definition, let’s think about a standard loss function from a machine learning model.

$$ \min_{\phi} L(X;\phi)$$

Typically, the goal is to minimize some loss function \(L\) over different parameters \(\phi\). Now, we can expand this loss function to accommodate a decentralized framework

$$ L(X;\phi) = \sum^{K}_{k=1}w_k L_k(X_k;\phi_k) $$

Here \(k\) indexes each local data source. Now, we are simply minimizing the weighted sum of local losses. Typically, this weighting \(w_k\) is given by the fraction of observations present at each hospital, but different weighting schemes can serve different purposes (more on this later).

It’s important to note that federated learning is huge field, with lots of different flavors and variations. What was described above, and what will be discussed in the remainder of this post is a specific kind that seems natural to many clinical applications. Specifically, these applications involve aggregating data from multiple hospitals, such that each node is a hospital, and each hospital stores mostly the same variables. To facilitate future searches, this method is called centralized federated learning (which is confusing, given that the alternative to federated learning is called centralized learning), using the FedAvg algorithm with a hub and spoke topology.

The first step is for the central server to share a model with each node. Then, models are trained locally before sending their parameters back to the central server.

The central server will then aggregate all the parameters, before sending the updated model back out to each hospital. This repeats until the model is trained.

To formalize this definition, let’s think about a standard loss function from a machine learning model.

$$ \min_{\phi} L(X;\phi)$$

Typically, the goal is to minimize some loss function \(L\) over different parameters \(\phi\). Now, we can expand this loss function to accommodate a decentralized framework

$$ L(X;\phi) = \sum^{K}_{k=1}w_k L_k(X_k;\phi_k) $$

Here \(k\) indexes each local data source. Now, we are simply minimizing the weighted sum of local losses. Typically, this weighting \(w_k\) is given by the fraction of observations present at each hospital, but different weighting schemes can serve different purposes (more on this later).

It’s important to note that federated learning is huge field, with lots of different flavors and variations. What was described above, and what will be discussed in the remainder of this post is a specific kind that seems natural to many clinical applications. Specifically, these applications involve aggregating data from multiple hospitals, such that each node is a hospital, and each hospital stores mostly the same variables. To facilitate future searches, this method is called centralized federated learning (which is confusing, given that the alternative to federated learning is called centralized learning), using the FedAvg algorithm with a hub and spoke topology.

Decisions and Considerations when Implementing Federated Learning

Before implementing any federated learning system, there are some precursor decisions you’ll have to make, as well some features of your data that should be quantified. Some of these decisions have standard solutions for the generic medical context (i.e. multiple hospitals, with mostly the same features, but different observations). For the few considerations that don’t have standard solutions, we’ll go over a set of common options in more detail.| Decision or Consideration | Description | Standard Solution in Clinical Setting |

|---|---|---|

| Nodes and Topology | How many nodes? Will there be aggregate nodes? How will they be connected? | Few nodes (each node is a hospitals), all connected to one aggregate |

| Updates | How many nodes will participate in each update? | All connected nodes will participate in updates |

| Data structure | Naming conventions, file structures, etc. | None, because it depends so much on the specific problem you’re working with. Here’s an example from neuroscience called BIDS |

| Data partitions | Are features, labels, or observations shared across nodes? | Each node will have different observations, but at least some shared features and labels |

| Data distribution | How are features and labels distributed across nodes, and how will this influence the learning algorithm? | Multiple (see below) |

| Privacy measures | What extra privacy measures will be taken, if any? | Multiple (see below) |

| Hyper parameters | Weighting coefficients (wk), loss function, etc. | Weighting by the number of observations, but there are some interesting and useful variants (see dealing with non-IID data for some examples). All other parameters determined similarly to centralized learning |

Dealing with Non-IID Data: The biggest technical issue on this list is probably 'data distributions'. The standard FedAvg algorithm discussed here is not guaranteed to work well when the data are not identically distributed (non-IID) across nodes – and is rarely IID across nodes in real-world settings. Quantifying how the distributions of data differ and adapting the algorithm to deal with those distributions is an important part of the process. Overall, there are three big ways that data can differ across nodes. Nodes can have missing values, nodes can have different distributions or proportions of values, or the same values can lead to different predictions in different contexts. When reviewing the literature, it seems like each of these different data situations has a unique name, however not everyone seems to agree on what that name is. I think you can understand everything in this post without the names, but for the purpose of searching the field, here are the common names I observed for these different data situations:

- Feature skew: some features not present. i.e. one hospital does not record heart rate.

- Label distribution skew: some labels are not present. i.e. building a model to predict COVID when one hospital has no patients with COVID.

- Concept Shift: the same features lead to a different label. i.e. building a model to predict gut health from cheese consumption with hospitals in Asia and Europe. Since lactose intolerance is more common in Asia, the 'cheese' feature would lead to different labels at different hospitals

- Concept Drift: or the same label arises from different features. i.e. building a model to predict anxiety levels in hospitals with patients from different socioeconomic levels. While both hospitals might have patients with anxiety, the things causing that anxiety might differ.

- Quantity skew: labels have different distributions (imbalanced). i.e. building a model to predict COVID when one hospital has 40% of patients test positive, and another has 2%.

- Prior probability shift: features have different distributions. i.e. using age as a predictor when data come from children's hospitals and general hospitals.

- Unbalancedness: vastly different numbers of observations. This one is self explanatory.

- Balancing training data: each node can implement its own resampling scheme, such as SMOTE or GAN resampling. In the same review mentioned above, this was the most popular method for addressing skew [3], though the review only discussed the first three methods in this list.

- Adaptive hyperparameters: using loss functions and weighting coefficients that are specific to each node.

- LoAdaBoost: one specific example that boosts the training of weak nodes by forcing the loss function to fall below some threshold before they contribute to the aggregate[4].

- Domain adaptation: Use meta-training to determine how to combine predictors trained on various domains, similar to transfer learning[5].

- Share data: share a small amount of data or summary statistics from data to fill in missing values and supplement skewed distributions

- Normalization: (only applied to deep learning models) group, rather than batch normalization helps with skewed labels[6].

- Different algorithm: Federated learning based on dynamic regulation (FedDyn) algorithm can guarantee that the node losses converge to the global loss[7].

Dealing with Privacy: Despite federated learning being more secure than centralized methods, federated learning is not free from privacy risks. Bad actors with access to the model can still reverse engineer data from the model parameters, and therefore gain access to sensitive information. This issue is more pressing when not all the nodes can be trusted – like when nodes are users cell phones rather than hospitals. Because of this, about half of clinical federated learning papers do not use additional privacy protections[3]. However, if you’re interested in adding extra security, there are two ways that people tend to increase security: adding noise, and encryption.

- Add noise: add noise to either the data, or the gradients

- Differential privacy: a method of adding noise that ensures that model outputs are nearly identical even if any one data point is removed.

- Encryption: encrypt the gradients or parameters that get sent back and forth

Python Packages for Implementing Federated Learning

If you’ve thought about the design of your federated learning pipeline and are ready to implement it, there are a few free packages in Python that can help you get your system up and running- PySyft

A screenshot from a PySyft tutorial

- Supports encryption and differential privacy

- Support for non-IID data (via sample sharing)

- ‘numpy-like’ interface (their words)

- Currently, they want users to work with the team on new applications

- Tensorflow

A screenshot from a tensorflow tutorial

- Probably easy to use if you already work with tensorflow

- No built-in support for privacy or non-IID data

- FATE

A screenshot from a FATE tutorial

- No support for non-IID data (though nothing is stopping you from adding your own resampling function to the pipeline)

- Supports encryption

- Pipeline package interface

Conclusions and Commentary

- Federated Learning promises a flexible, decentralized way to train machine learning algorithms. Widerspread adoption of federated learning could make modeling with more sophisticated methods, or for more niche populations feasible

- Federated learning is presented as a solution to data governance and privacy issues that make sharing data difficult. While the method has clear benefits over centralized learning, data privacy, and especially data governance, will likely still present issues moving forward. As discussed in the post, federated learning applications are not a complete solution to security issues and will likely require more protections in any real-world application. Additionally, the incentives that make it harder for institutions to contribute data to data lakes might also make it harder to offer access for federated learning projects. If you spent a lot of money collecting a rare dataset, you might want to get the first (or second, or third) crack at any modeling projects using that dataset. Essentially, I do not think federated learning can serve as a substitute for incentivizing data sharing or protecting/compensating data curators.

- Starting a federated learning project requires many decisions and considerations. Decisions with the least clear solutions are those involving data standardization across sites and those involving how to deal with non-IID data distributions. Both reviews cited in this post recognize that these are important issues[1,3], but stop short of providing clear recommendations. I think the method would be more accessible and more likely to be used responsibly if some of the packages produced pandas-profiler style reports of data distributions across sites and provided more support for implementing solutions.

References and Resources

- Rieke, N., Hancox, J., Li, W., Milletarì, F., Roth, H. R., Albarqouni, S., Bakas, S., Galtier, M. N., Landman, B. A., Maier-Hein, K., Ourselin, S., Sheller, M., Summers, R. M., Trask, A., Xu, D., Baust, M., & Cardoso, M. J. (2020). The future of digital health with federated learning. Npj Digital Medicine, 3(1).

- Schwarz, C. G., Kremers, W. K., Therneau, T. M., Sharp, R. R., Gunter, J. L., Vemuri, P., Arani, A., Spychalla, A. J., Kantarci, K., Knopman, D. S., Petersen, R. C., & Jack, C. R. (2019). Identification of Anonymous MRI Research Participants with Face-Recognition Software. New England Journal of Medicine, 381(17), 1684–1686.

- Prayitno, Shyu, C. R., Putra, K. T., Chen, H. C., Tsai, Y. Y., Tozammel Hossain, K. S. M., Jiang, W., & Shae, Z. Y. (2021). A systematic review of federated learning in the healthcare area: From the perspective of data properties and applications. In Applied Sciences (Switzerland) (Vol. 11, Issue 23). MDPI

- Huang, L.; Yin, Y.; Fu, Z.; Zhang, S.; Deng, H.; Liu, D. LoAdaBoost: Loss-based AdaBoost federated machine learning with reduced computational complexity on IID and non-IID intensive care data. PLoS ONE 2020, 15, e0230706.

- Guo, J., Shah, D. J., & Barzilay, R. (2018). Multi-Source Domain Adaptation with Mixture of Experts

- Hsieh, Kevin; Phanishayee, Amar; Mutlu, Onur; Gibbons, Phillip (2020-11-21). The Non-IID Data Quagmire of Decentralized Machine Learning". International Conference on Machine Learning. PMLR: 4387–4398.

- Acar, Durmus Alp Emre; Zhao, Yue; Navarro, Ramon Matas; Mattina, Matthew; Whatmough, Paul N.; Saligrama, Venkatesh (2021). Federated Learning Based on Dynamic Regulation

- For a lighter read, check out this comic from Google

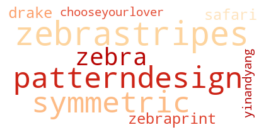

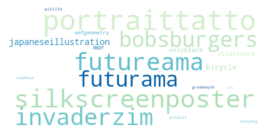

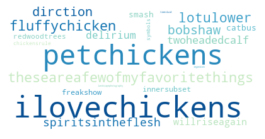

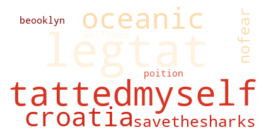

Coastal differences in artists' Instgram captions

A network analysis of tattoo pieces, September, 2022

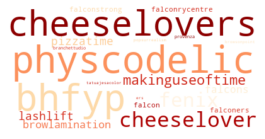

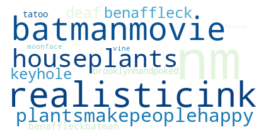

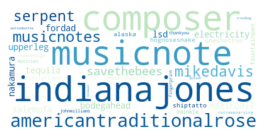

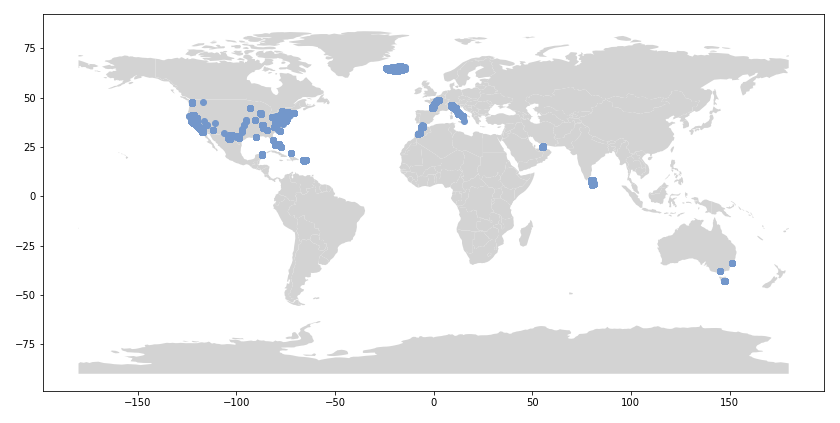

To me, tattoos seem like a great way to express autonomy, aesthetics, and interests all in one place. I'm always interested in hearing peoples tattoo stories, and my Instagram feed is usually about 70% images of fresh ink on any given day.

Recently I've wondered what sorts of stories I might be missing by limiting my exposure to hyper-curated algorithms and people I already know.

In short, I wanted to do a broader survey of the tattoo landscape. If I could pull enough data and do some statistical clustering, I could potentially sort through a much larger swath of the tattoos than I would normaly be exposed to.

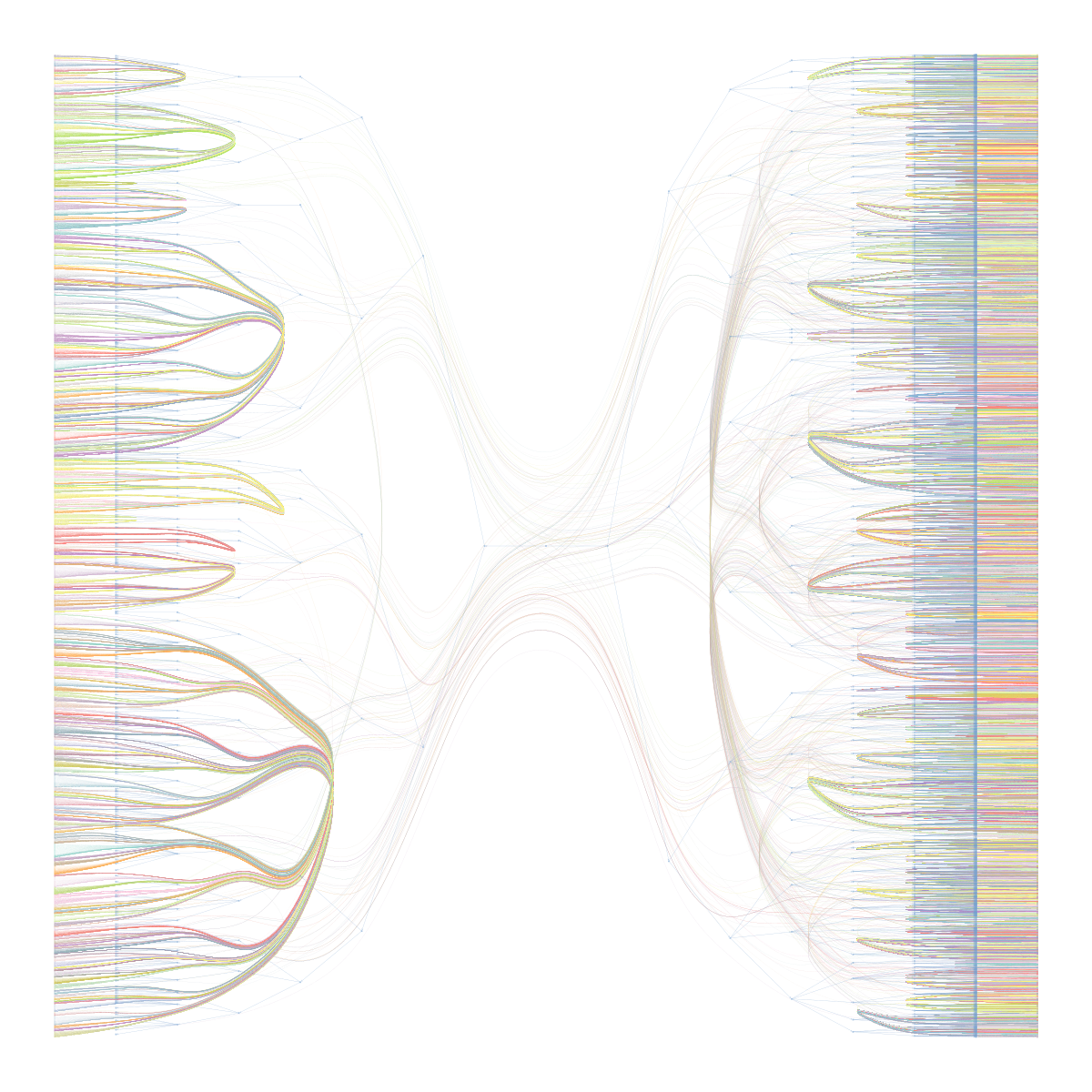

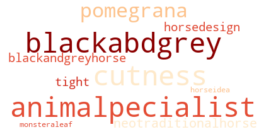

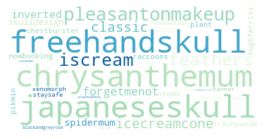

Specifically, I wanted to answer a few questions: What are the most common tattoo styles and subjects?

How do these differ geographically in the US? If I can get descriptors of each tattoo, what are some prominent groupings of tattoo descriptors? Do those groupings differ in different cities? And, are there any interesting groups I haven't been exposed to so far?

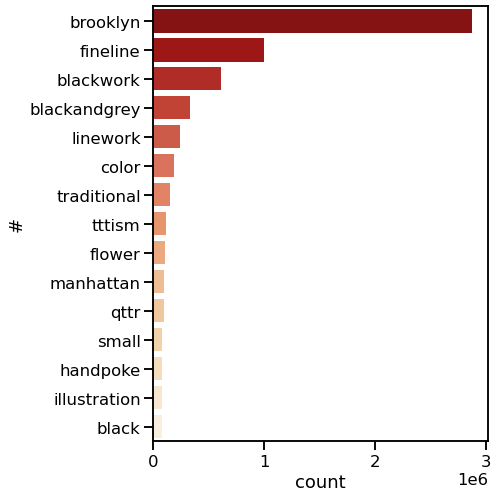

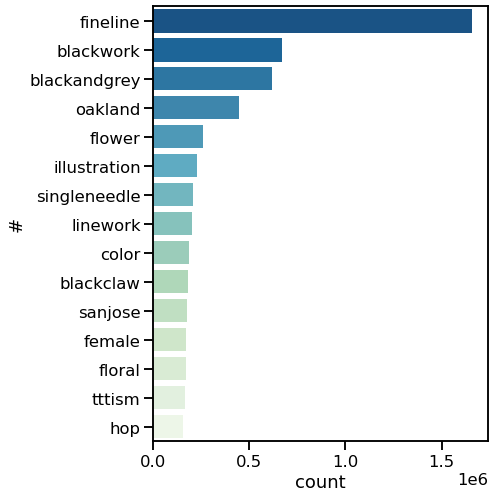

I decided to use Instagram posts to collate a dataset of tattoos, and to use hashtags from each post as markers of style, content, or other tattoo features. As a simple assessment of geographic specificity, I pull two datasets: one from San Francisco (SF) and one from New York (NY).